To understand National Security Group (NSEC), we must analyze the two equally important parts of this insurance operation - the underwriting and float allocation. The underwriting is a crucial part to determine the cost of float, as a company that has a low cost of float will consistently have underwriting profits and a company that has an expensive float will in turn consistently have underwriting losses. This concept is relatively similar to banking where you preferably want non-interest bearing deposits or extremely low cost deposits to in turn lend out to get a good spread and thus make money on other people's money. The leverage of the up front and tax-free cash given by policy holders is the use of float which will also be analyzed.

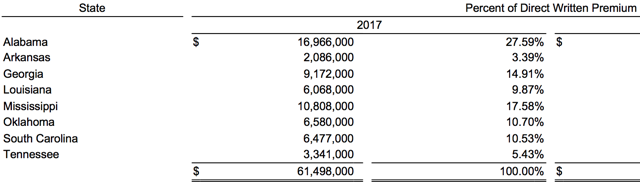

Detailed Background on the UnderwritingThe company primarily does dwelling insurance around the Gulf Coast. The company is currently concentrated in the Gulf Coast as shown below:

The company is slowly diversifying away from the Gulf region as shown with the premium volume in Oklahoma, Tennessee and Georgia. This trend will continue, although at a somewhat slow pace as the competition to write business in those states may become unfavorable and writing business for unfavorable policies in order to fulfill a diversification target could be extremely costly. It is important to note that a home owner's insurance policies for the customer in Alabama would be more expensive than a home owner's insurance, for example, in Nebraska as the probability of a claim in Nebraska is lower as there obviously are no hurricanes in the Midwest to cause home damage. The average home owner's annual rate in Nebraska is $1,583 compared to Alabama where the rate is $2,134. So writing home owner's insurance for claim-prone states like Alabama, Mississippi and Louisiana isn't necessarily riskier than writing business for a state like Nebraska. The company also has a small life insurance segment that makes up around 10% of total policies and gives NSEC an added leg to hold up the chair. I would note that last year the company had a difficult year in underwriting, as did many insurers as a result of the unusually high amount of claims due to the extremely active storm season. However I am extremely confident that the unusually bad 2017 storm season that gave NSEC a net loss is unlikely to become a consistent pattern. Another added cushion that NSEC has [thus making it a conservative investment] is the reinsurance policy they have, which covers up to 2 events in each calendar year that exceed $4 million in claims. So NSEC would still bear the liability of the first $4 million, yet the reinsurer would bear any added liability [over $4 million].

Detailed Background on Float/Capital AllocationThe float, which in my view is a terrific asset, could turn into a big negative if investments are poorly allocated and cause losses. Another thing that slightly negatively impacts float is the low interest rate environment that we are in. Having said that, the majority of the company's fixed income securities mature within the next 5 years, which better positions the float in case interest rates rise. When/if interest rates rise, the value of the bonds will go slightly down as a result. Yet as long as the company does not sell the bonds, potential losses will always be unrealized. I want to reiterate that I have no clue on where interest rates will be 3 or 5 years from now. But I do think it is important to be cognizant that we are in a low rate environment in historical terms.

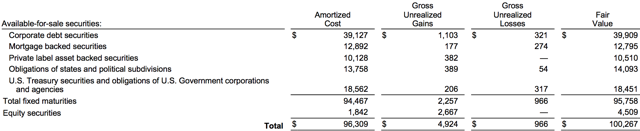

Below is the present allocation of the float:

The float, which is composed of corporate debt and government related debt, is decently allocated. I am a little disappointed with the current float composition as I would prefer to see much more equities in the float rather than debt investments as equity investments, such as low cost index funds, will generally outperform over the long term compared to fixed income. Part of the reason for the lack of equities is the regulators do have control in limiting equity allocation.

In ConclusionI do believe that the intrinsic value of NSEC is greater than its current market cap of $39.4 million/$15.60 per share. A rough guidepost of looking at intrinsic value is the book value of $46 million/$18.53 per share. I want to reiterate that book value is an extremely rough starting point to get to intrinsic value, as the real determinant of a company's value is how much cash it can generate from now to forever. In my view the intrinsic value is a little above book value, as I believe that low cost float will slowly grow along with a slow diversification from the Gulf Coast, which will in turn increase net income over time. However I want to reiterate to readers that I do think the company is bound to have some annual losses as a result of the occasional strong storm season. Yet those losses will not be very often and mitigated due to the reasoning I gave in the underwriting background. So you will need a stomach for volatility at the occasional time there is an underwriting loss.

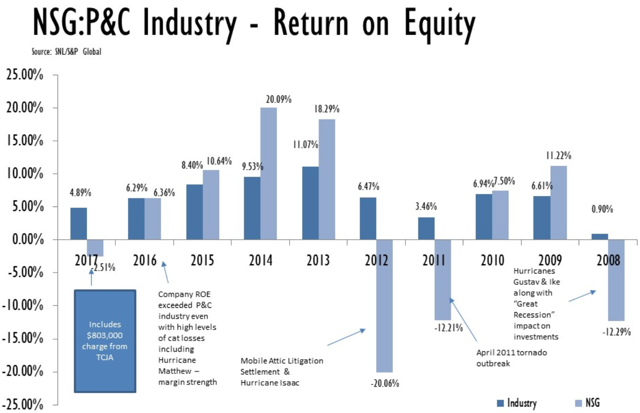

In the above table you can see the volatility with net income and net losses, which is largely associated with their Gulf Coast concentration and a one-off litigation settlement from a former investment. However, over the last five years, NSEC achieved a 9% annual growth in book value. I do want to stress that if one bought this stock for just a year or two they may lose money, but for the very long term investor this will be a good purchase.

I am thrilled to be a shareholder of NSEC and plan to be one for many years to come.

Disclosure: I am/we are long NSEC.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor's Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

LPTH Revenue (TTM) data by YCharts

LPTH Revenue (TTM) data by YCharts LPTH data by YCharts

LPTH data by YCharts

(Data from 11/'16 analysis)

(Data from 11/'16 analysis) (Data from 03/'18)

(Data from 03/'18)

News stories about BB&T (NYSE:BBT) have been trending somewhat positive on Friday, according to Accern Sentiment Analysis. The research firm ranks the sentiment of news coverage by analyzing more than 20 million blog and news sources in real-time. Accern ranks coverage of publicly-traded companies on a scale of negative one to positive one, with scores nearest to one being the most favorable. BB&T earned a news sentiment score of 0.16 on Accern’s scale. Accern also assigned news articles about the insurance provider an impact score of 46.6887882598231 out of 100, indicating that recent news coverage is somewhat unlikely to have an effect on the company’s share price in the near future.

News stories about BB&T (NYSE:BBT) have been trending somewhat positive on Friday, according to Accern Sentiment Analysis. The research firm ranks the sentiment of news coverage by analyzing more than 20 million blog and news sources in real-time. Accern ranks coverage of publicly-traded companies on a scale of negative one to positive one, with scores nearest to one being the most favorable. BB&T earned a news sentiment score of 0.16 on Accern’s scale. Accern also assigned news articles about the insurance provider an impact score of 46.6887882598231 out of 100, indicating that recent news coverage is somewhat unlikely to have an effect on the company’s share price in the near future.