LightPath Technologies, Inc. (LPTH) is an infrared, diversified optics company with a future focus on autonomous vehicles/AV. Their Lidar products are utilized for AV.

The micro-cap stock is trading with a market capital around $52 million; a near 52-week low around $2 price per share. The bottom support, P/E value among peers, and the decent volume could pair well with steady revenue growth. A DIY investor could pick up shares at a value if willing to risk the uncertainties of a micro-cap stock.

LightPath Tech holds market research showing that 2021 will bring key adoption for autonomous vehicles, thus increased demand for sensors (Lidar, ADAS, etc.). Their research shows the growth from, "$2.5 billion in 2016 to nearly $4.6 billion by 2021, a 5-year CAGR of 12.6%." - 12/'17 LightPath Press Release

The aforementioned 2021 timeline coincides with Ford Motor's (F) launch of its autonomous vehicles in Florida:

According to the Q1 2018 Ford earnings transcript, Ford will operate autonomous vehicles in Florida by end of 2021. This will be a partnership with Domino's Pizza and Postmates. - The Swift FCF Yield

The following analysis will look at three aspects:

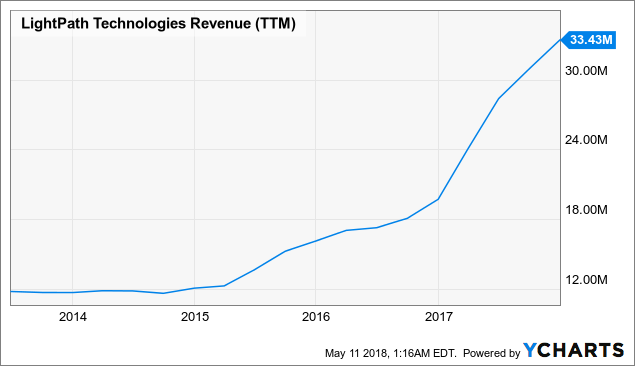

LightPath's better appeal among micro-cap peers utilizing FinViz screener Cash on hand and FCF Yield A review of past interests/concerns from 11/'16 LightPath analysis LightPath Revenue Growth +5% SequentiallyWhen locating a stock at year lows, it can be safe to assume there is distress. On top of the average concerns, an investor could expect revenue is on the decline. This is not the case with LightPath Tech.

LPTH Revenue (TTM) data by YCharts

LPTH Revenue (TTM) data by YCharts

When running a stock screener, LightPath Technologies is found by choosing: (1) stocks under $300m Market Cap, (2) under 15 P/E and forward P/E, and (3) "sales growth past 5 years" of over 5%.

The company's price to earnings P/E is 6.8. When comparing the Q/Q sales growth for the past 5 years, there is an increase of 24.47% CAGR (Q3 2013, $2,846,718; Q3 2018, $8,503,628).

The stock price action has had two previous spikes over the course of 3 years.

LPTH data by YCharts

LPTH data by YCharts

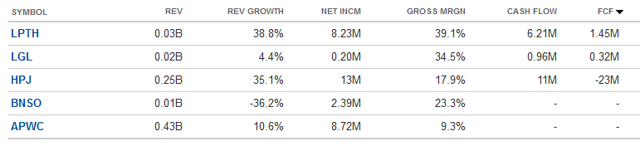

LightPath Technologies is within the Industrial Electrical Equipment industry and only a few micro-caps are listed. By using similar screening values in P/E, the comparisons are:

| Highpower International, Inc. (HPJ) | 3.5 P/E |

| Asia Pacific Wire & Cable Corp. (APWC) | 4.0 P/E |

| Bonso Electronics International, Inc. (BNSO) | 6.7 P/E |

| LightPath Technologies, Inc. | 6.8 P/E |

| The LGL Group, Inc. (LGL) | 109 P/E |

Overall, LightPath Tech has showed a low support formation around the $2 price per share. When looking for a growing micro-cap, the company appears to be of fair value with decent P/E and consisted revenue growth. Cash on hand and analysis of debt is also important to consider.

LightPath Tech FCF Yield

At the end of Q3 2018, LightPath Tech had $6.4m in cash and equivalents on hand, which might seem low. However, the cash flow, CapEx, and FCF are better handled than comparable micro-caps as shown in the Seeking Alpha chart below.

When the FCF is compared to the market capital for a yield, we arrive at approximately 0.33%. The yield is low, but at least positive. CapEx is elevated with investments in R&D, namely autonomous vehicle tech.

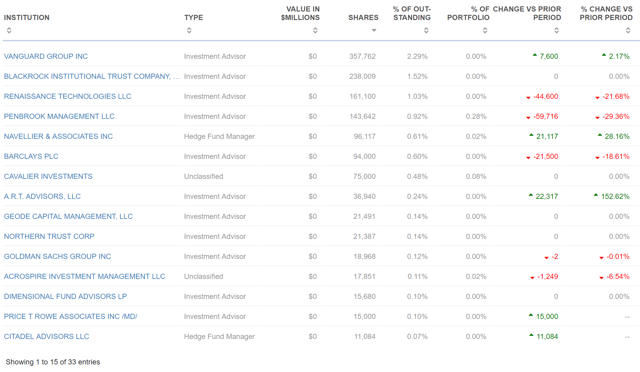

Update On Past AnalysisIt was November 2016 when Dallas Salazar last analyzed LightPath Technologies in "LightPath Technologies/ISP Optics M&A..." At that time, the institutional ownership was charted in the image below.

(Data from 11/'16 analysis)

(Data from 11/'16 analysis)

One of the risks at that time was the willingness for institutions to buy a micro-cap with a low price per share that had just taken on more expenses with a recent M&A. The next chart shows the most recent institutional ownership.

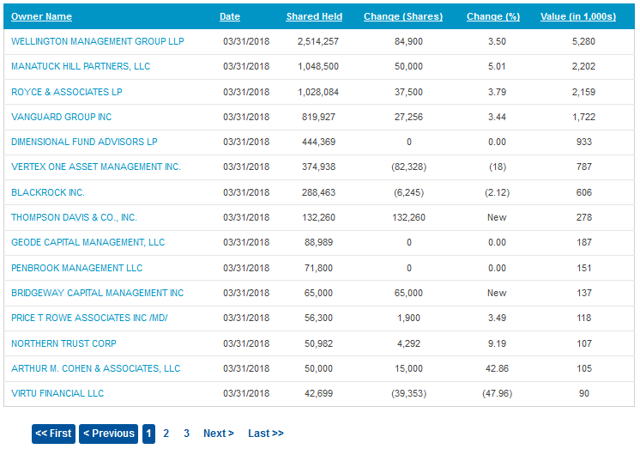

(Data from 03/'18)

(Data from 03/'18)

There are several changes to point out. Vanguard Group Inc. was once the largest institutional holder by share volume with 357,762 shares. That has since increased to 819,927 for a 129% jump, but they are no longer the largest holder.

Wellington Management Group LLC has $453,768m in market capital and they hold the largest share volume of LightPath with 2.5 million shares. Manatuck Hill Partners LLC and Royce & Associates LP each own over one million shares.

Among these shareholders, five have more than doubled their position. The largest movement was by Dimensional Fund Advisors LP, which increased by a multiple of 27 going from 15,680 to 444,369 shares.

LightPath Tech Valuation BenchmarksAnother comparison from the former analysis in November 2016 is Enterprise Value/EV. At that time, the price per share was around $1.50 and the EV was approximately $20m. Salazar had projected a 100% upside with a $41.5m target EV. As of May 2018, the price per share hovers near $2 and the EV is $61m.

A new conservative price target can be arrived by using discounted Q/Q or Y/Y sales growth of 15% CAGR and then a price to sales valuation. For example, we know that a 5-year, Q/Q sales growth is at 24.47% CAGR. If a conservative estimate of a flat $8m can be seen for Q4, then there will be a 2018 total sales of approximately $32.5m. This would give us a 5-year, Y/Y sales growth of 22.5% CAGR. Using a 15% CAGR for projection seems reasonable.

The current P/S ratio is approximately 1.66, which would give us about a $2.43 PPS target for 2019 if no dilution. For 2021, the P/S valuation would be about $3.22 PPS, again with no dilution. The return on investment now could yield over 50% with a 3-year horizon, 17% for a 1-year horizon. I think the 3-year conservative horizon can be beat with successful integration into the AV market.

RisksFirst, the company tends to have a backlog and yet it is also growing into other markets such as autonomous vehicles. This backlog is viewed as a positive by the company, "As a result of our strong bookings performance in the third quarter, our 12-month backlog was approximately $12.9 million in March 31, 2018, an improvement from $12.3 million at the end of the second quarter and $9.3 million from the beginning of the fiscal year."

The concern is if this micro-cap can scale and compete versus larger companies? Is it susceptible to larger companies taking its customer base when it is unable to fulfill orders at faster rates?

Second, the company states in the Q3 10-Q Form that it has increased its assets abroad, namely China. "As of March 31, 2018, we had approximately $14.7 million in assets and $12.6 million in net assets located in China, compared to approximately $14.0 million in assets and $12.3 million in net assets located in China as of June 30, 2017."

The concern is the timing of the U.S. Administration's tariff struggle with China and the limitless negative reciprocity that may come with it. There is a risk that LightPath Tech could find operating in China more expensive in seasons to come or that repatriation of the cash to carry great loss.

A third concern is the history of dilution for supporting inorganic growth. Last time, December 2016, Roth Capital and underwriting partners picked up 8 million shares at $1.21 PPS. This was used to finance the acquisition of ISP. Moving ahead into Autonomous vehicles/AV could also require similar financing and dilution.

ConclusionAutonomous vehicles/AV is a growing market with a benchmark of 2021. It is of interest to be a shareholder of a smaller company that could grow substantially due to said advancement. The low price per share of LightPath Tech presents as an undervalued stock for the patient retail investor. This stock is rated a buy.

Disclosure: I am/we are long LPTH, F.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor's Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

No comments:

Post a Comment